Voluntary Carbon Market, what 2024 brought us

2024: A Year of Milestones and Momentum in the Voluntary Carbon Market (VCM)

An important mechanism in global climate action

As detailed in our article on the year 2024, the voluntary carbon market demonstrated significant growth and resilience last year, proving that it remains an important mechanism for global climate action.

The year was marked by a search for integrity and the emergence of new norms and standards, such as the Core Carbon Principles and the evolution of CORSIA eligibility criteria, both in terms of standards and methodologies.

All these initiatives augur well for the future, but when it comes to analyzing the past year and the current state of the voluntary carbon market, one factor remains paramount: withdrawals from registries.

As a reminder, a withdrawal is the removal of a carbon credit from a registry in order to offset a tonne of CO2e emitted. Once withdrawn, a carbon credit can no longer be sold. A tonne of CO2e emitted can therefore only be considered as offset once the carbon credit has been withdrawn from the registry.

What’s more, the list of withdrawals is public, unlike the act of purchasing carbon credits itself, which is mostly carried out via private, over-the-counter contracts. In fact, to assess potential market demand, the quantity of carbon credits withdrawn from private registers is a good indicator of total demand, but does not reflect the full reality. Indeed, many customers buy carbon credits with recent vintages and choose to retire them later (banking), in order to benefit from wholesale prices or low price opportunities on certain projects.

It is interesting to study withdrawals in order to quantify the emissions that have actually been used by end buyers (notably companies that contribute to the global effort to reduce and eliminate emissions beyond their value chain). It is an indicator of real demand on the voluntary carbon market, as it excludes players who buy carbon credits to trade them or for a potential speculative approach.

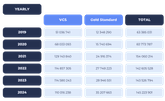

To get a clearer picture of the past year and the current state of the voluntary carbon market, we looked at the withdrawals from the two historical standards: VERRA (hereafter VCS) and Gold Standard (GS).

In total, in 2024, over 110 million credits were withdrawn from the VCS registry and over 35 million from the Gold Standard registry, bringing the total for both registries to over 145 million offset tCO2e. To properly analyze this figure, we need to put it into perspective with the withdrawals of previous years.

This total of 145 million is the second highest since 2019 (2021 having accumulated 154 million withdrawals). 2024 marks a slight increase on 2023 (+1.2%). For Gold Standard, the total withdrawn is even the highest since the creation of the standard.

This initial analysis shows that the carbon market continues to prove its resilience and growth potential.

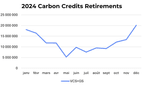

One thing is certain: there are major disparities from one month to the next.

As the graph above shows, there is a gap of over 284% between the “quietest” month (May, with around 5 million tonnes withdrawn) and the most active (December, with over 20 million tonnes withdrawn).

Generally speaking, the months closest to the end or beginning of the year are the most active. 2024 got off to a strong start, with an active January and February. This was followed by a dip in May, then a rise in June, followed by stabilization, until the December peak.

Withdrawals are therefore irregular over the years, but do they follow the same trend from year to year? Well… not really. There are a few constants, however: December is almost always the busiest month, and if it isn’t, it always marks a sharp acceleration compared with the months that preceded it.

The usual end-of-year peak is explained by the reporting calendar of companies. In fact, companies generally report their carbon footprint in February or March of year N+1, for year N emissions. Some purchase carbon credits just after this calculation, but in all cases, they have until December of year N+1 to withdraw their credits and offset their emissions.

However, the December peak is lower than in 2023, when more than 25 million credits were withdrawn. Although irregular, withdrawals were more evenly distributed than last year. Whether this is a genuine underlying trend or a one-off phenomenon, however, we’ll have to wait and see the analysis of withdrawals in 2025.

For the rest of the year, however, it’s hard to discern any real trend. Generally speaking, the third quarter is quieter than the others, but there are a few exceptions. Even so, it seems that a buyer looking to offset his emissions would be well advised to make his purchase during this quarter, in order to benefit from less competition and, therefore, better conditions.

To conclude this section, it should be noted that the day with the most withdrawals on Gold Standard was December 3 (~1.3 million withdrawals), while for VCS it was December 17 (~4.5 million withdrawals, i.e. almost as many as for the whole of May).

In terms of locations, the “historic” countries of the carbon market are represented: China, India, Brazil and Turkey. We also note the presence of two African countries on the GS side and one on the VCS side, two of which belong to the United Nations list of Least Developed Countries.

In the Gold Standard, the vast majority of credits come from renewable energy and waste management projects, or community projects (access to water, improved cooking stoves, etc.).

This figure demonstrates the strong co-benefit aspect that remains associated with Gold Standard-certified projects.

VCS continues to play a key role in nature-based projects. Renewable energy and waste management projects also continue to dominate the credits withdrawn in 2024.

Of the 5 projects with the most withdrawals in 2024, 4 are REDD+ projects (Reducing Emissions from Deforestation and Forest Degradation in Developing Countries). The project with the most withdrawals has 9 million credits withdrawn. REDD+ projects remain key offset projects. Despite media controversy, customers remain committed to these forest preservation projects. This should be seen as good news, as it is essential to preserve existing carbon sinks, and because these projects bring strong social co-benefits (involvement of local communities in the project, generation of sources of income replacing those that could be obtained by deforesting…) and biodiversity benefits (maintaining the habitat of endangered species, preserving native species…).

2024 was an active year in which the voluntary carbon market proved its resilience. With more than 145 million credits retired from the two historical registries, even as ICROA-certified standards become more numerous, the trend is clearly one of growth.

That’s good news, because if we are to meet the Paris Agreement target, massive investment will be needed. For example, additional funding of $10 billion a year is essential to develop quality projects such as reforestation and mangrove restoration (Source: UNEP State of Finance for Nature 2021 report).

Article written by :

Carbon Offset Buyer